》View SMM copper quotes, data, and market analysis

》Click to view the historical price trend of SMM spot copper

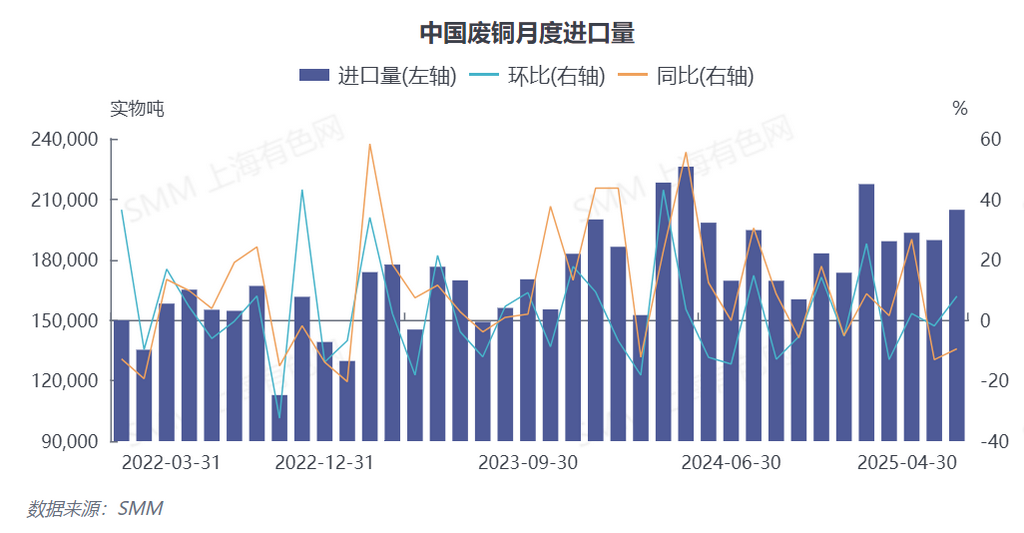

The latest data from the General Administration of Customs (GAC) shows that in April 2025, China's imports of copper scrap and shredded copper scrap exhibited a trend of "MoM recovery but YoY contraction," with monthly imports reaching 204,700 mt, up 7.92% MoM but down 9.46% YoY. From January to April, cumulative imports totaled 777,000 mt, a slight decrease of 0.81% YoY (HS code 74040000).

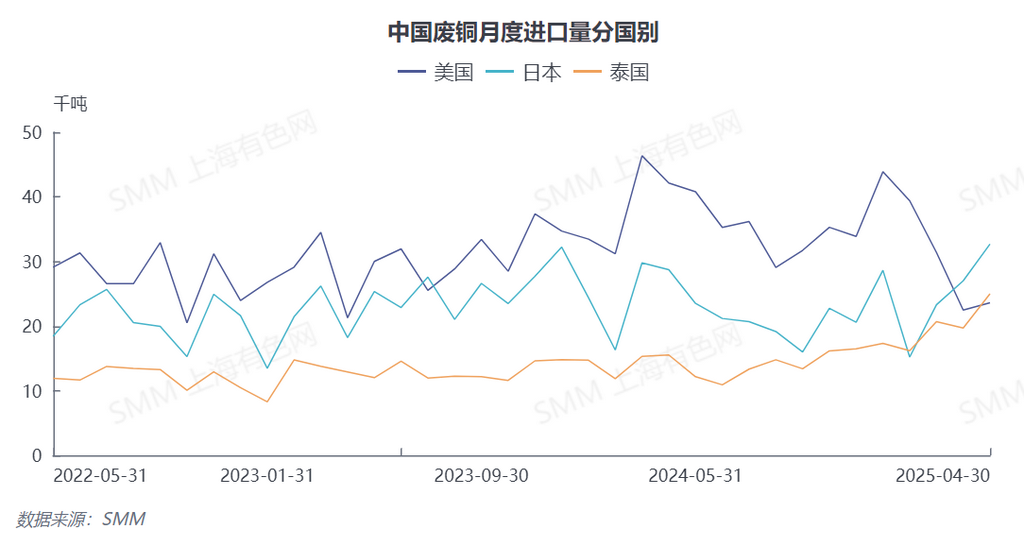

I. Drastic Changes in Regional Patterns: A "Three-Kingdom" Drama of the US, Japan, and Thailand

Looking at the breakdown of import sources, there has been a significant shift in the current structure of import sources, with traditional dominant player, the US, continuing to cede market share. Data from March-April shows that US copper scrap exports to China exhibited characteristics of "double declines": in March, exports were 22,500 mt (down 28.41% MoM and 51.51% YoY), with its market share in China dropping to 11.85% and its ranking falling to second place; in April, although exports increased slightly by 4.98% MoM to 23,600 mt, they still fell sharply by 43.98% YoY, with its market share further shrinking to 11.52% and its ranking being overtaken by Thailand, falling to third place.

In stark contrast is the strong rise of the Asian supply chain. Japan's exports to China reached 32,700 mt in April, up 21.02% MoM and 13.78% YoY against the trend, securing the top spot with a 15.96% share. Additionally, the Thai market saw exports of 25,000 mt that month, surging 26.9% MoM and 60.98% YoY, becoming the second-largest supplier. The synergy of the Asian regional supply chain is becoming increasingly prominent.

II. Aggravation of Structural Shortages, Dual Pressures from Policy and Market

Looking ahead, according to SMM, the current supply of secondary copper raw materials in the market remains extremely tight, with both domestic and imported sources in short supply. Despite the continued market demand, many traders are actively seeking ways to import secondary copper raw materials, but overseas offers are scarce, making it difficult to achieve large-scale purchases. Furthermore, affected by Trump's tariff policies, traders generally reject US sources, which are more likely to be absorbed in local markets such as Japan and Thailand. In the coming months, imports are expected to maintain a trend of "declining volumes but rising prices," with the market shares of Japan and Thailand expected to exceed 18% and 14%, respectively, while the US share may fall below the psychological threshold of 10%. (The following presents import data by country for March-April 2025.)